Let me ask you a question. How much will your long-term care cost?

The answer, of course, is you have no idea. You may be one of the lucky ones who is completely independent and dies of "natural" causes in their sleep. Or you may be diagnosed with early onset Alzheimer's and need expensive care for a number of years. It's not unusual for people to spend up to $20,000 per month on long-term care (I've got family experience).

It's often said that LTC Insurance is for the middle class - the poor can rely on Medicaid to pay for care and the wealthy can pay for care themselves. But is self-insuring, or to be more precise self-funding, always the best choice?

When polled in 2022, Americans said a net worth $2.2 million would make them feel wealthy. You may feel if you reached that milestone at age 65 you could retire comfortably and draw down your wealth at the "classic" 4% level. If you encountered long-term care expenses, you would then accelerate the amount you spend - and choose which assets to liquidate as needed.

This all makes sense and chances are that person starting with $2.2 million wouldn't become completely broke from LTC needs - though it is a possibility. So, the rational decision, and one that many financial advisors recommend, is to not buy LTC Insurance and instead self-fund the cost. One wealth manager thinks that saving $225,000 for LTC needs should be adequate.

For many this is an easy decision. People can't envision needing long-term care and they are confident that their healthy lifestyle will prevent them from getting Alzheimer's or other chronic conditions. Plus, they may have heard LTC Insurance is expensive for what you get.

Self-funding for care is an easy decision. However, is it the right one?

Before a you decide that you will self-fund, it is valuable to discuss what you should be prepared for. Here are some:

-

Dealing with Loss Aversion. In the same way that it is less painful to whip out a credit card for a $100 dinner as opposed to laying out $120 cash, spending money from a brokerage account every month to pay for care will be more difficult than having a third party (i.e. LTC Insurer) pay those costs. Can you visualize making these monthly care payments?

-

Impact on Care Choices. Similarly, imagine shopping at two stores. One of the stores has full retail price on every item and only accepts cash. The other charges an annual membership fee, but discounts every item at 80%. This is similar to the experience of someone having LTC Insurance. The policy gives you the comfort of purchasing additional services because much of the care is paid for by the policy.

-

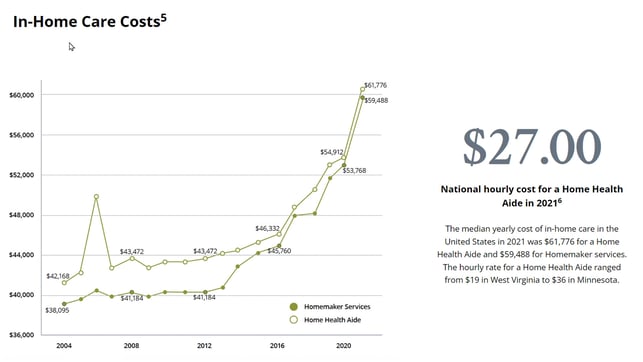

Underestimating the cost of care. Care costs can be tricky to estimate and range widely by geographic location. In the last couple of years the cost of home care has increased dramatically. According to Genworth in their care trends study, the cost of home care increased 12.5% in 2021. Core Inflation, immigration and demographics mean this trend is likely to continue into the future.

-

Timing and liquidity of self-funding. For people who choose to self-fund their care it is critical that they identify those assets they would use for care. They don't want to be in a situation where they have to sell investments or real estate in a down market. So there is no misunderstanding, it's recommended that people complete and sign with their advisor an asset identification form that tells people where the funds for care will be found.

-

Tax Considerations. Another consideration is taxes. What are the tax implications of withdrawals for paying for care? Retirement planning includes considerations on the most tax efficient withdrawal strategies to avoid higher tax brackets and expenses. Will LTC expenses paid then be deductible as medical expenses, subject to the 7.5% of AGI rule? A benefit of LTC Insurance is that benefits payments are typically tax-free. This tax guide can explain some of the tax treatment of LTC Insurance.

- State Payroll tax exemption. Recently Washington State implemented the nation's first publicly funded LTC plan for all state residents. The plan is funded by a .58% state payroll tax - so someone earning $200,000 would pay an annual tax of $1,160 to fund a plan that would provide a maximum benefit of one year of care. For people who had private long-term care insurance prior to November of 2021 they were able to opt out of the tax. Will other states follow Washington and develop their own state plans? It is possible in several states, and preparing clients now will help the conversation.

-

Family Considerations. For people who self-fund, they may want to consider having a family discussion about what the plan for care would look like, what assets are designated for use and what the implications may be for adult children who may be planning on an inheritance one day. Often the desires and finances of siblings may be very different, not to mention that daughters can often bear the brunt of coordinating care. Often a care event can both force a family together but also create underlying family problems at the same time. Families who are insured with LTC Insurance find that children appreciate the planning that went into the purchase of the product and now have a 3rd party to help with care coordination as well.

-

Protecting the tail risk. At extreme, some care events can be very expensive. A 10-year severe disability requiring 24 hour care could exceed $2,000,000 in costs. This could disrupt other planned uses for savings. As a way to protect against this, there are LTC insurance policies with lifetime coverage options.

- Leaving a charitable legacy. Charitable giving is very important to many people. If they are envisioning leaving a legacy to a particular cause or causes, how will a LTC event impact those plans?

Long-Term Care Insurance can be an option to self-funding worth considering. Here are some types of LTC Insurance in the marketplace today:

1. Traditional LTC Insurance

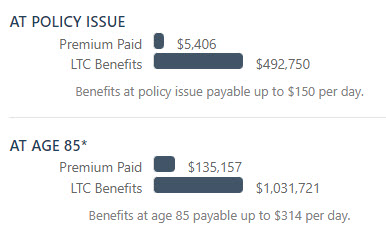

Traditional LTC Insurance provides some of the purest protection and leverage in paying for care. The product is pretty straightforward - premiums are paid and if you need care a pool of money is available to help. Here's an example of the economics for a 60 year old couple:

As you can see, in this example for a combined premium of about $5,000 there is a pool of money to pay for care of about $500,000 that will inflate each year at 3% compound. By the time care may be needed at age 85 a combined pool of over $1,000,000 is available for care.

As you can see, in this example for a combined premium of about $5,000 there is a pool of money to pay for care of about $500,000 that will inflate each year at 3% compound. By the time care may be needed at age 85 a combined pool of over $1,000,000 is available for care.

Traditional LTC policies offer the most leverage for premium dollar in LTC coverage.

2. Hybrid Life/LTC Policies

Hybrid Life/LTC policies combine life insurance with a rider for LTC coverage. The products are based on permanent life policies such as whole life, universal life, indexed universal life and variable life. In addition to the LTC Insurance, Hybrid plans offer a death benefit and cash surrender values. It's often said live, die or quit you'll get policy values.

The three benefits available: death benefits, cash and surrender benefits, and LTC benefits - can vary greatly by carrier, product, and plan design. It is a competitive marketplace with many options to select from.

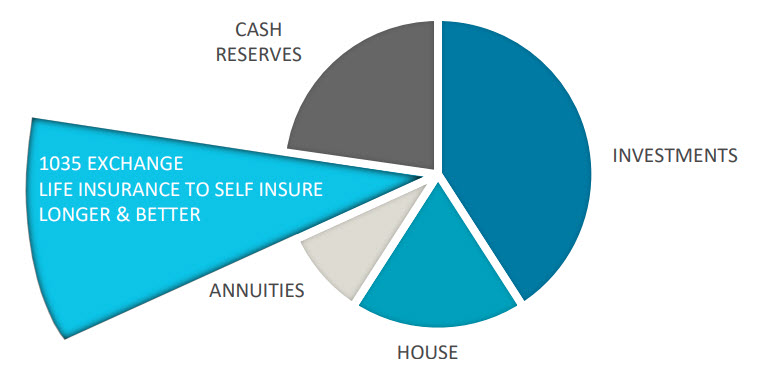

There are many ways to pay for a Life + LTC policy. They can be paid through a single premium, premiums over 10 years of premiums paid for a lifetime. A popular option is to fund a policy through a 1035 exchange of an existing life policy. This greatly increases the amount of money available to pay for care as illustrated below.

3. Annuity/LTC plans

For those who have non-qualified annuity out of a surrender period, a 1035 transfer and purchase to an annuity/LTC plan can both leverage the annuity value from 2 to 3 times plus allow for tax-free withdrawals to pay for care. Annuity/LTC plans also can help reposition a safe asset into another safe asset that also leverages for a care event.

4. LTC Riders on permanent life insurance

Individuals with life insurance needs for estate planning can select policies that accelerate the death benefit if LTC is needed. Typically, these plans don't include inflation protection coverage. It's important to consider the implications of what a reduction in death benefit through a LTC acceleration will mean for the overall plan.

Investigate the options, choose a plan - and monitor that plan periodically.

Planning for LTC might seem difficult. After all, it is uncomfortable to think about and requires thoughtfully thinking through the consequences a care event would have, not just on you, but your spouse, your children, and overall legacy planning. But it doesn’t have to be difficult.

Before assuming you are willing and able to self-fund those consequences, it makes sense to engage in a dialogue with your financial advisor regarding your options. The more "normal" interest rate environment makes LTC Insurance more affordable, and several carriers have reduced premiums on plans. The longer you wait to plan, the fewer the available options. A great way to start is by completing an initial health prescreen to see if insurance is even an option for you.

Consumer Guide