Recently I had a great experience of participating in a one-day conference at New York University in which a group of academics tried to get the answer to a simple question - what's holding back the LTC Insurance market in the United States? The conference featured participants from schools like NYU, University of Chicago, Stanford, Duke and others. There were also attendees representing insurers, government agencies, and researchers from LIMRA, Fidelity and Vanguard.

"Why aren't more people buying LTC Insurance?" It's the type of question that might be featured on a Freakonomics podcast - a need so great should create a robust market- but recent sales have been disappointing while in-force policy management by carriers has been challenging (and not very profitable).

Did the conference succeed in identifying the main reason for the market problem? The simple answers is no. However, there were several promising ideas put forward that should result in future research and help produce concrete suggestions.

One thing everyone at the conference agreed with - in the absence of any changes the United States is facing a "two-tiered" long-term care system - one in which the wealthy can get paid professional care through private pay and LTCI, while everyone else will rely on friends, family, charity, and a challenged Medicare and Medicaid system.

The focus of this session was on private sector market issues, including regulatory issues. With federal action very unpredictable due to current political conditions in DC, there was an emphasis on possible state actions for LTC Insurance reform, including smarter regulation and faster approvals of rate increases and new products. The National Association of Insurance Commissioners have submitted ideas to congress recently for improving the private market.

Among the several discussions and presentations, I found four areas of interesting discussions that may lead market changes and increased sales:

-

Should carriers consider offerings plans that trigger benefits on the loss of more than 2 of 6 ADL (activities of daily living) benefit triggers?

It may surprise some people, but as a percentage of the population France has a larger private LTC market than the United States, and several carriers participate. What is the secret to their success? The conference included representatives from insurance carriers that participate in the French marketplace, such as AXA. Those representatives implied that a reason for their success may be the fact that French LTC policies typically have more stringent benefit triggers than the LTC plans sold in the US. In France, most policies require a loss of 3 of 4 ADL's, and any cognitive impairment needs to be more severe than US policies to trigger benefits payments. More stringent benefit triggers mean, of course, that it is harder to qualify for benefits BUT it also means that premiums will be lower and insurance carriers can predict claims with more accuracy.

For those who have been in the LTC Insurance business for awhile, we remember the days of deciding between "non-qualified" versus "qualified" LTC Insurance. Back then many proponents of non-tax qualified LTC thought that the HIPAA based qualified benefit triggers were TOO restrictive and that triggers such as "medical necessity" should be part of LTC benefit triggers. In fact, Penn Treaty, one of the leading LTC carriers, sold a lot of "non-TQ" plans on this basis. It's now apparent those liberal triggers may have benefited policyholders but it came at a big cost. Penn Treaty has been liquidated, and one of the causes were paying more claims than anticipated.

So the question is - could a carrier offer a plan with a 3 of 6 ADL benefit trigger and maintain the tax-qualified status of LTC Insurance? A reading of IRS Section 7702b about the treatment of qualified long-term care insurance says that in order to be a chronically ill individual someone has to be unable to perform at least 2 of 6 activities of daily living. It doesn't say policies can't use more than 2. Perhaps carriers and state regulators will look at the possibility of LTC policies that may be "harder" to qualify for - focusing on paying for professional care and offering a lower premium to buyers.

-

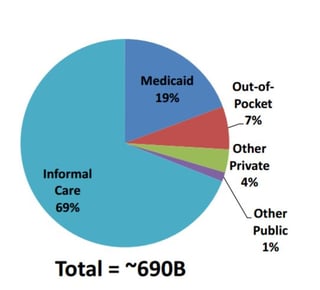

Is informal care crowding out the need for formal paid care?

Informal care by friends and family is the biggest part of caregiving today - up to 69% of the economic value of care being provided. Many people who have not planned for paying for care must rely on informal care. Of course, this "freely" provided informal care has great costs, not least of which is removing many Americans from being employed in other jobs and adding to the economy. John Phillips of the Social Security administration pointed out that many retirees social security benefits are impacted because of lost earnings during working years. A law professor from UCLA, Allison Hoffman, discussed a proposal that any possible future government LTC Insurance solution should pay for both formal care for those needing care and help the caregivers with income supplements. A costly proposal, for sure, but an thoughtful way of looking at LTC as a family issue.

The good news is that many of today's plans from carriers like Mutual of Omaha and Transamerica include a cash alternative, normally a percentage of the formal (professional) care benefit. These cash plans can help ease the burden of lost income for caregivers.

-

Can hybrid solutions go "downmarket"?

Hybrid Life/LTC plans are very familiar with financial advisors and popular with affluent clients, but less familiar to regulators and academics. Representatives from companies like Lincoln Financial pointed out some of the attractive features of hybrid plans that exist side by side with health based standalone products. Hybrid products can have unique benefits for both carriers and buyers.

For carriers, hybrid products include the "skin in the game" aspect of the policyholder funding the premium - which means at claim time they are taking their own policy contributions first before the "insurance" part of the plan kicks in. From a consumer perspective, the benefits of hybrids include guaranteed premiums and, if LTC benefits aren't used, a death benefit or return of premium. The downside to hybrid plans for many is the premium expense - but longer duration premium payment options can help with that.

-

What's the future of the group LTC market?

Voluntary worksite sales are increasing, and LTC Insurance can be a growing way for people to buy coverage. The advantage of worksite LTC products include unisex pricing and underwriting concessions. Several trends in worksite LTC show promise for the future.

First, a couple of standalone carriers have had success selling individual products at the worksite and it is anticipated that more standalone carriers will offer worksite products. Next, the built in tax advantages of worksite plans for employers have been well documented and more employees have Health Savings Accounts and can use pre-tax dollars to buy coverage. Linked life/ltc carriers are exploring the market and should be rolling out plans in the near term. Finally, as discussed above, the NAIC long-term care sub-committee is recommending that qualified funds be allowed to be withdrawn penalty free to pay LTC premiums - both promoting the purchase of coverage to help protect retirement savings and ease the possible burden on Medicaid.

Thinking of the LTC Insurance market as under performing and finding ways to fix and improve it will be critical for both families and the country as a whole. Careful improvements could actual lead to dramatic changes in planning, and it is encouraging that serious study is underway.